|

CHAPTER 2

THEORETICAL FOUNDATION

2.1 Accounting Information System (AIS)

Accounting

information

system (AIS)

is

a

system that

collects,

records,

stores

and

processes data into an accounting information that will be used for decision making in

an

organization (Romney,

Steinbart, 2006).

According

to

Gelinas,

to

meet the

established goals, we can measure from the effectiveness of AIS (Gelinas, 1990).

However, “AIS can be

in a

form of

manual or computerized system. Regardless of the

type, AIS is designed to collect, enter, process, store, and report data and information

“(Salehi et al, 2010).

According

to

Wilkinson

et

al,

accounting

information

system is

a

“

structure

exist

in

entity that employs physical resources and other components to transform economic data

into

accounting

information

with

a

purpose of

satisfying

needs

of

variety

users”

(Wilkinson et al, 2000)

“

AIS

is

consist

of three

major

subsystems:

the

transaction

processing

system,

the

financial reporting system, and management reporting system” (Hall, 2008). Each

subsystem of

AIS

has

a

different purpose such as, the

transaction

processing system

(TPS) mainly support daily business operation with numerous reports, documents, and

messages for users throughout the organization. Financial reporting system is producing

traditional

financial statements that

usually required by the law such as

income

7

|

|

8

statement, balance sheet, statement of cash flows, tax returns, and other reports that may

related. Lastly, management reporting system providing internal management with

special purpose financial report and information needed for decision making such as

budgets, variance reports, and responsibility reports (Hall, 2008).

2.2 Accounting Information System documentation

As discussed earlier, AIS processing data into information that will be used by users for

decision-making. AIS is documented in several form, such as Data flow diagram (DFD),

document flowchart, system flowchart, and program flowchart. AIS documentation tools

will be discussed as follows (Romney, Steinbart, 2009):

1. Data flow diagram:

Data flow diagram (DFD) describe the flow of data within an organization, it shows the

source and the destination of

the data or, and also describe the entire process and data

storage.

2. Document flowchart:

Document

flowchart

describes

the

flow of

documents

and

information

between

departments within an organization.

3. System flowchart:

System flowchart describes the relationship between input, output and processing within

information system

|

9

4. Program flowchart

Program flowchart provides information about sequences of operation that is performed

by computer and executes program.

5. Entity relationship diagram

Entity relationship diagram illustrate

the graphical technique

for portraying a data

base schema. It shows the relationships between entities and how these entities are

being modeled

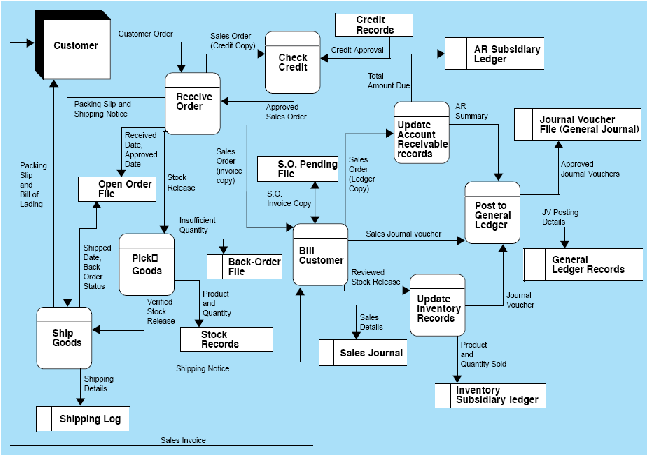

Table 2.1 Data Flow Diagram of sales process based on

Accounting Information

System

|

10

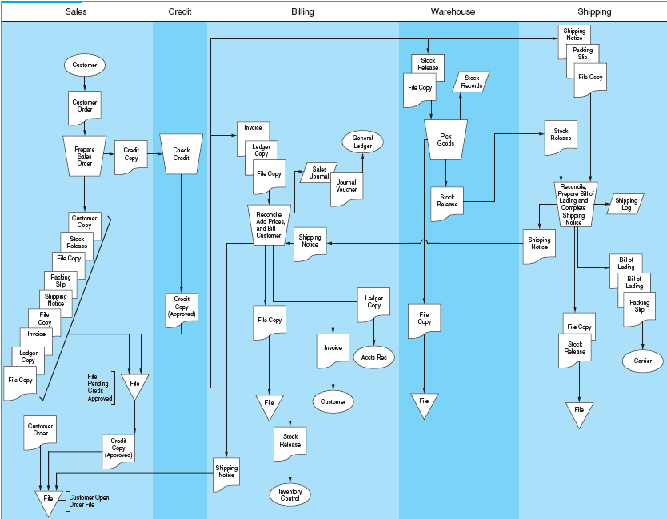

Table 2.2 Data Flowchart of Sales Process based on Accounting Information

System

|

11

Billing

Inventory Control

ACcounts Receivable

GeneralLedger

Updale General

ledger from Journal

Vouchrs

and

Reconcile

|

12

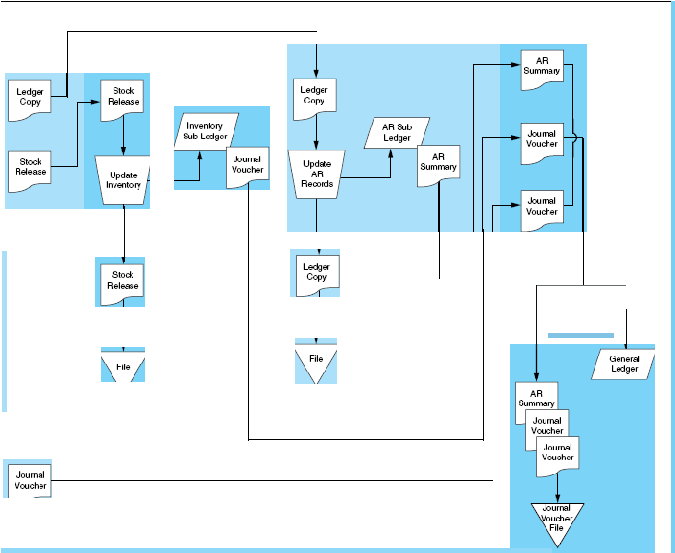

Table

2.3

Data

Flow

Diagram of

Cash

Receipts processes

based on

Accounting

Information System

|

13

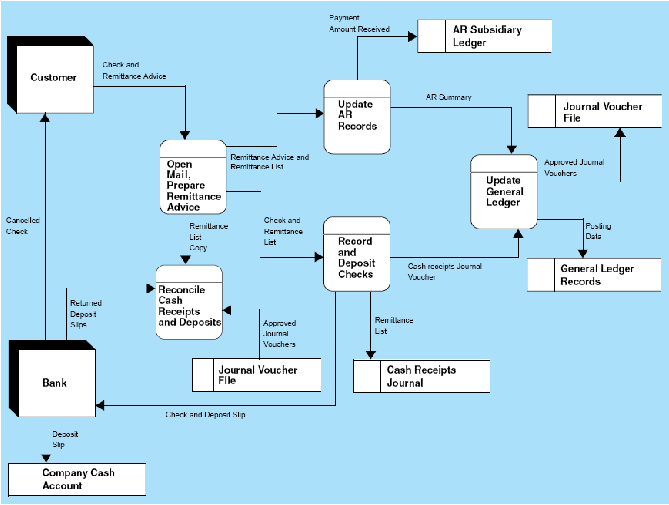

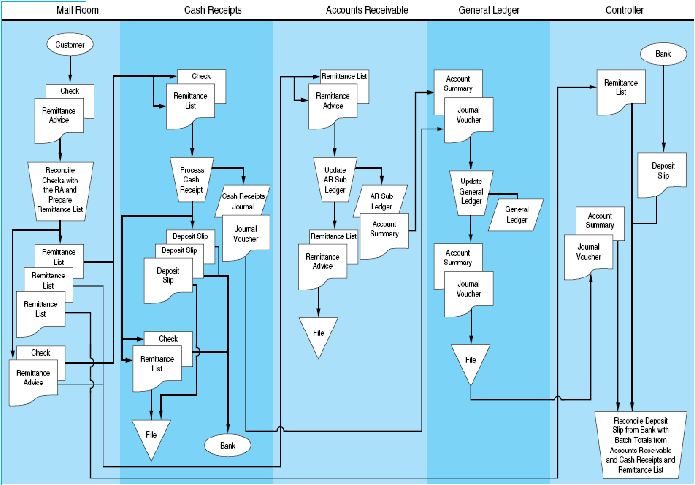

Table 2.4 Data Flowchart Cash Receipts processes based on Accounting

Information System

|

|

14

2.3 Revenue cycle

2.3.1 Definition of Revenue cycle

Revenue is the income of the company derived from the business activities such as sale

of goods and services, revenue is usually collected after customer received the goods or

the

services

has

been

performed by the company. In the financial report, revenue

commonly recorded as “sales”.

Furthermore, Revenue cycle is a “business activities and information processing, which

brings about the providing of goods or services to customers and collecting payment in

terms of cash” (Romney, Steinbart, 2006).

Revenue cycle consist of two major subsystem:

1. Sales Order Processing, which includes tasks such as:

•

Preparing sales orders

In this process, customers will send purchase order, which lists the goods

that are going to be ordered. Sales order will be prepared, this document

provide information about customer’s account number, description of

orders; and the quantities and unit price of each item.

•

Check credit

Before

further

process of customer’s

order, sales department

will check

the

creditworthiness

of

the

customers. This

is

done

to

ensure

that

the

customers have the ability to pay.

|

|

15

•

Shipping products to the customers

Goods

are

shipped

to

customers

after all the procedures have been

properly done. Warehouse department will prepare the goods and the

shipping clerk reconciles the physical items with the stock.

•

Billing customers and properly record the transaction

Customers will be billed after the shipment of goods has been completed.

Billing

customers

before

the

completion

of shipment

will

result

in

inaccurate records.

2. Cash Receipts, which includes tasks such as:

•

Collecting cash from customers

Cash are collected from customers after the billing procedures have been

completed. It is important to ensure that the cash collected have matched

with the amount that should be paid by the customers.

•

Depositing cash in the bank

Cash

is

deposited

in the

bank

after collection

has been completed.

By

depositing the cash, it will ensure that cash are kept in safe place.

•

Adjusting between the payment and the customers transaction

Accounting clerk reconcile between bank record and customers

transaction. This is done in order to check whether customers have paid

the transaction according to the actual amount.

|

|

16

•

Properly record the financial transaction

Financial transaction has to be properly recorded after all the procedures

have been properly done. Accounting

department will update account

receivable ledger and also general ledger.

2.3.2 Revenue cycles control

There are six classes of internal control within this cycle:

1. Transaction authorization:

The

main

objective

of

this

control

is

to ensure that all transactions should be

properly authorized and only valid transaction that can be processed further. In

order to

implement this objective, the

use of credit check, return policy

system

and remittance list is applied to the system. Credit check is to check the

creditworthiness of the

customers and

make sure

that

they are

feasible

(Hall,

2008).

2. Segregation of duties:

Segregation of duties

is

very

important,

this to ensure that no individual or a

department have the authority over control or access all the business processes.

Segregation of functions consists of three rules:

|

|

17

1. Transaction authorization should be separate from transaction processing:

In

this

system,

the

credit

authorization

is being segregated

from all the

processing, this

means

that authorization and transaction processing

is

separate

events.

2.Asset custody should be separate from asset record keeping:

It

is

very

important

to separate asset custody

from the asset

record

keeping

as

to

ensure the assets is keep safe . a person with combined responsibility could steal or

lose inventory and adjust inventory to conceal event.

3. The organization should be structured that perpetration of a fraud requires

collusion between two or more individuals:

The task of

recording

transaction

has

to be

structured

and

carefully

separated.

Subsidiary ledger, journals and general ledger have to be separated between each

other. By separating the tasks,

there will

be less risk in the company and it

is

easier to detect fraud.

Supervision:

Supervision is a form of control in company in which to ensure that all the workflow

is properly done. As according to (Hall, 2008), supervision is often used when

it

is

unable to conduct an appropriate segregation of duties.

|

|

18

Accounting Records:

Accounting records

act

as

an

audit

trail

and

it

is

very important

to

be

properly

maintained,

so

it

will

be

easier to keep track of every process and to find errors

occurred in the system. By using pre numbered documents can keep record of every

single events in the process and it will be easier to identify each documents.

Access controls:

Access controls is crucial for the control of the revenue cycle as when there is no

limited access to certain areas it can lead to fraud action. In revenue cycle, assets that

most needed to be protected are cash and inventories; access to accounting records

such as account

receivable

subsidiary

ledger and

cash journal

has

to be

narrowed

(Hall, 2008).

Independent Verification:

Independent verification is to ensure

that all procedures and accounting

records

is

being reviewed by

the system as to having an assurance in

terms of accuracy and

completeness.

2.3.3 General structure of good revenue cycle management system

Nowadays

many companies are

unable to survive due to the

lack of management skill.

Revenue cycle is one of the most critical components of the management. Therefore, a

good revenue cycle management is highly needed in the organization. Guyton and Lund

had listed four characteristics of good revenue cycle

management system, they are

(Guyton, Lund, 2003):

|

|

19

1. Better information management

Management has to be able to provide real time information as to make sure

the accuracy of data. Every business process

has to be properly documented,

thus, it will improve information management within organization.

2. Tighter accountability

Designing revenue cycle based system for the business operation is important

in order to increase control as well as accountability. However, implementing

revenue cycle based system is not enough, segregation of duties is also highly

needed as to make control become tighter. Lastly, it is suggested for company

to

implement performance-based management

information

system to support

accountability of the company

3. Reduced variability

Automated workflow and approvals will increase efficiency of the company,

as

there

will

be

no paper

work,

all-business process

is

properly recorded.

Managers also need to actively monitor and measure the overall performance.

4. Comprehensive integration

Firstly, in order to increase comprehensive integration, company should

conduct analysis on revenue cycle system and also concentrate on

functions

that considered being critical.

Secondly, company has to encourage controls and policies through rules and

regulation. Lastly, it is recommended

for

company

to

have

automated

workflow and leverage relationship with partners.

|

20

2.3.4 Threats and Controls in the Revenue Cycle

(Romney, Steinbart, 2009)

Table 2.3.4. Threats and Control of Revenue Cycle

Process

Threat

Control Procedures

Sales Order Entry

1. Incomplete

/

inaccurate

customer

orders

2. Credit Sales to poor

credit customers

3. Legitimacy of orders

4. Stock outs, carrying

costs, and markdowns

1. Data entry checks

2. Credit approval

by

manager,

not

by sales function

3. Signature on

paper document

4.

Inventory control

systems

Shipping

5. Shipping Error:

Incorrect merchandise

Incorrect quantities

Wrong address

6. Theft of inventory

5. Reconciliation

of

sales

order with

picking ticket and

packing slip;

barcode scanner

6. Restrict

physical

access

to

|

21

inventory,

physical count of

inventory,

RFID

barcode

technology

Billing & A/R

7. Failure

to

bill

customers

8. Billing errors

9. Posting errors in A/R

7. Separation

of

shipping

and

billing functions

8. Data

entry

edit

controls; price list

9.

Reconciliation of

subsidiary A/R

ledger

with

general ledger

Cash Collections

10. Theft of cash

10.

Segregation

of

duties,

minimization

of cash handling

General Control Issues

11. Loss of data

12. Poor performance

11. Back up and

access control

12. preparation

and review of

performance

|

|

22

report

2.4 Internal Control

2.4.1 Definition of Internal control

According to Hermanson as cited from Institute of Internal Auditors, internal control

defines as a set of controls that is designed by the management to provide assurance

that the company meet the following objectives (Institute of Internal auditors, 1993),

such as:

1. Reliability and integrity of information

All information in the company is reliable and trustworthy. High

integrity of

information

is

needed as to ensure

that

information being

used is accurate.

2. Compliances with laws and regulations

Internal control implemented in the company has to be

in accordance

with laws and regulations. In this way, it will increase the value of the

company.

3. Safeguard of assets

Assets of the company are usually at high risk, therefore strong

internal control is highly needed in order to protect company’s asset.

|

|

23

4. Efficiency of operations

Efficiency of operations is one of the most important objectives, as by

increased

in efficiency

will

affect

the

overall

performance

of

the

company.

5. Accomplishment of goals

Goals

of

company

are

ensured that

it

has

been successfully

accomplished; this measures the overall performance of the company.

Internal control and business risk are interrelated between each other as it represents a

critical component of corporate governance framework, and this become the primary

mechanism through which organization manage their business risks. Moreover,

internal control is use as the primary by the organizations to minimize the probability

of reaching company’s goal (Wong, 2000).

According

to

Noordin,

“there

are

wide range

definitions

of

internal

control. In its

broadest sense, internal control refers to both administrative and accounting controls”

(Noordin, 1997).

1.

“Administrative control consists the plan of the organization; methods and

procedures that help the management and planning control activities”.

2. “Accounting control consists all methods and procedures that are mainly focused

on authorization of transaction, safeguarding of asset, and the accuracy of the

financial report. Strong accounting controls will increase efficiency and decrease

both data error and fraud”.

|

|

24

There are four objectives of internal control system, which are (Hall, 2008):

•

Safeguards assets of the firm:

Internal

control

system

protect

assets

of

the

firm

from

damage,

loss

and

fraud, this is done by properly check the assets and matched it with the asset

records.

•

Ensure accuracy and reliability of organization’s accounting data:

Internal control system is

responsible to check the accuracy and make sure

that all accounting data is reliable. By having a systematic check on every

accounting data it will minimize on misinterpretation or data error.

•

Promote efficiency of the firm:

Internal control help promote the efficiency of the firm as the internal control

is implemented, there will be an

increase

in the

efficiency of the operation,

thus it will bring a profitable behavior to the firm.

•

To

measure compliance

with

management

prescribed

policies

and

procedures:

Internal

control

system measures

whether

all

business

process

have

been

complied with the management policies and required procedures.

|

|

25

2.4.2 Components of internal control

Based on Committee of Sponsoring Organization (COSO) under SAS 78, there are five

main elements of internal control, they are:

1. Control Environment:

Control environment

is

very

important

for the development of the

internal control,

according to COSO guidance, there are 7 principles of control environment.

Those

principles are:

•

Integrity and ethical values

Integrity

and

ethical

values

have

to

be built and

developed, and

understood particularly on top of management,

so

the

business

environment will have high integrity and ethical values which will result

in better company performance. Rules & regulation on financial reporting

have to be set according to accounting standards (Arens et al, 2006).

•

Commitment to competence

“Competence is the knowledge and

skills

that

is required

to

fulfill tasks

for individual job. Commitment to competence includes the consideration

of

the management towards

competence levels

for

specific

jobs”

(Arens

et al, 2006). Requisite skills and knowledge are being translated from the

levels of competence.

|

|

26

•

Board of directors or audit committee participation

Independent of management is considered to be the characteristic of an

effective board of directors, and the members is involve in all

management’s activities. The board has to conduct a regular independent

assessment for the management’s internal control, by having this

assessment,

the

internal

control

of the

company

will

likely

to

perform

better. In addition, the board with high objectives will effectively reduce

the possibility of overrides existing controls. However, the audit

committee is also having responsibilities such as, maintaining

communications with both external and internal auditor, approval activity

of both audit and non-audit services performed by the auditors of public

companies.

Moreover,

directors and auditors

will

evaluate

issues

related

to integrity and management’s actions (Arens et al, 2006).

•

Management’s philosophy and operating style

The

information

about

importance

of internal control

is

delivered

to

employees through the activities of the management. In this way, strong

internal control would likely to

be

achieved

when

there

is

enough

understanding about the philosophy and also operating style of the

management (Arens et al, 2006)

|

|

27

•

Organizational structure

“Organizational

structure

contributes to

an

entity’s

ability to

meet

its

objectives by providing an overall framework for planning, executing,

controlling, and monitoring activities”(Leung et al, 2004)

•

Assignment of authority and responsibility

Employees are assigned an appropriate levels of authority and

responsibilities

as

to support the implementation of

internal

control

systems, thus goal of efficiency can be achieved (Gramling et al, 2007).

•

Human Resource policies and practices

Personnel play an important role in the implementation of internal

control. High competence and honest personnel is highly needed in order

to achieve efficiency and successful control system. Incompetent and

dishonest personnel will lead to a failure in the control system, thus the

business are unable to reach their goals. (Arens et al, 2006)

2.

Risk Assessment:

Management has to be concern about possibilities of risk and think of an action that

are necessary to overcome the risks. It is recommended for organization to identify, and

analyze about factor that may increase the risk. By having risk assessment, it will help

the company to reduce minimize the risk

|

|

28

3.

Control activities

Policies and procedures have to be established by the company as to ensure the

company to achieve their objectives. There are 5 types of control which support

the development of control activities, those control are:

1. Segregation of duties

“

Segregation

of

duties

ensures

that

an individual does not perform

incompatible duties. When a person commit an error in his work and be able

to conceal

the

error

it

is

considered as

incompatible

duties”

(Leung

et

al,

2004)

2. Proper authorization of transaction and activities

Every transaction and processes should be properly authorized in order to

have

a

strong

control.

None

of

transaction

can

be

processed

if

no

authorization is occurred.

3. Adequate documentation and records

Management has to ensure that documents are adequate for both transaction

and recording activities. Documents provide control over assets and

transaction activities.

|

|

29

4. Physical control over assets and records

Assets and record

have

to be properly

maintained as these two components

are

mostly

at

risk.

When

there

is no

adequate

protection

over

assets

and

records, they might be damage and loss, such event will disrupt the operation

of the management (Arens et al, 2006)

5. Independent checks on performance

Independent check is use to review the work performance of employees. By

having this review, the management will be able to identify any unintentional

mistakes done by the employees, thus high quality control can be achieved.

4. Information and communication

Information and communication system is maintaining accountability of assets

and responsible for the whole record, process and finally reporting the business

transaction (Arens et al, 2006).

5. Monitoring

Avellanet

point

out

that

Monitoring

is

a

set

of

procedures

that

provide

information’s about how internal control should be conducted (Avellanet, 2009).

Management should have monitoring, as it will assess the quality control that has

been

implemented.

Monitoring

usually

done periodically, and it has to be done

properly

as

to

ensure

the

operation

of internal

control

as

intended

by

the

management (Arens et al 2006)

|

|

30

2.4.3 Characteristics of Good internal control system:

Based on Noordin’s (1997) work, he listed eight characteristics of good internal control

system in which an organization might be use to appraise any procedures or transactions,

those characteristics are:

1. Reliable personnel with clear responsibilities:

Personnel play an important role in internal

control. In order to achieve a

successful internal control, high competence

and

honest

individual

is

needed,

otherwise, a good internal control can’t be achieved and there will be a

possibility

that

the system might

be spoiled.

High

competence personnel

will

increase productivity and minimize fraud.

2. Separation of duties:

Separation of duties will increase the accuracy of data as well as minimizing the

fraud. Elements of separation of duties are listed below:

a. Separation

of

operational

responsibility

from

record

keeping

responsibility:

This element refers to the separation between accounting functions and

operating department.

b. Separation of the asset custody from accounting functions:

This activity will

minimize

the

risk and

fraud. For example: cashier

should

not have access to the accounting

ledgers, and book keeper

should

not be

able to handle the cash (Noordin, 1997).

c. Separation

of

the

authorization

of

transaction

from custody

to

related

asset:

|

|

31

Independent

activity between

these

2

processes

will

increase

control

which

will reduce in data error or risk that may related to these activities.

d. Separation of duties in accounting functions:

Every individual should handle different tasks in the accounting department;

one

person

will

not

have

the

authority to

do

all

the

recording

process

throughout all transaction.

3. Proper authorization:

Every processes and transaction in the organization have to be properly

authorized. Ease of controls likely to be achieved, as it is easier to check if there

is

any

error

occurred,

the

supervisor

is able

to

check

from the

authorized

documents.

4. Adequate documents:

Every

transaction needs

to

have

an

appropriate

documentation

and

it

is

also

recommended that every document should be renumbered.

5. Proper procedures:

Every procedure

in the company

has to be made clear and

appropriate.

Procedures provide information about flow of documents and guidance for

record keeping. It is crucial for the company to have proper procedures, so it is

easier

to

track

control

of

every documents

and

processes

that

run

by

the

employees.

6. Physical safeguards:

Inventories and cash are the assets that are high in risk. In order to minimize the

risk

and

losses,

company

should

provide

limited

access

to these

assets,

only

authorized personnel that can access to this function.

|

|

32

7. Independent check:

Periodic review by both external and internal auditor is recommended for

checking the entire systems. The review should be conducted by a personnel who

has

no

direct

contact

with

the

processes, so

as

to

make

sure

that

the

report

produced by the auditor is reliable.

8. Cost benefit analysis:

Implementing control system in the organization is quite costly; it is suggested to

have an analysis in both cost (disadvantages) and benefit of the system.

2.5 Internal controls in Information Technology

2.5.1 Definitions of Information Technology (IT)

Based on Information Technology Association of America (ITAA), information

technology defined as "The design, development, implementation, and management

of computer-based information systems, particularly software applications and computer

hardware".

Nowadays large companies are relying most on information technology

to access

information,

and

especially

processing

and

storage of data.

Alexander point out that

Information technology is an important tool to manage the transactions, information and

knowledge required to expands every aspect of activities (Alexander, 2008).

2.5.2 Control issues in IT environment

The

use of

information

technology

has

increase efficiency in the business operation.

However, in order to keep the efficiency, there

has to be control

activities that able to

|

|

33

control the whole operation of

the IT system. Philee and Philee suggested

four simple

ways that can be implemented by all employees, these are (Philee, Philee, 2009):

1. Use of encryption:

Encryption is tools or software applications that protect important and

confidential

information

from unauthorized

personnel.

By

having

encryption,

there will be more control towards information as

unauthorized personnel

will

not be able to access the data.

2. Data restoration:

Data in the company are mostly at high risk. It is recommended for all employees

to provide back up for all data in the company. Restoration minimize the lost of

data.

3. Virus protection software:

In order to protect data and important information in the company, it is important

to protect computer with virus protection software as to prevent lost and damage

to files.

4. Passwords:

The use of passwords in every business process will limit the access to data and

software,

in this way, only authorized personnel

will be

able

to have access

to

related data and application.

Refer to Green et al 2006,

Data and information

in IT environment are assets of the

company. Unauthorized personnel who made intentional changes to data and

|

|

34

information is a critical issues for the management. Therefore, strong internal control is

highly needed in the information technology in order to meet objectives, as follows:

•

Integrity

relates

to the

completeness, accuracy,

and

authorization

of

information and systems:

Every

information

and

system process

has

to

be

clearly

authorized

by

the

management

and

ensure

the completeness and

accuracy of

the

data. Accuracy

includes valuation, presentation, validity and timeliness.

•

Confidentiality

Confidentiality

refers

to

protecting important

and

confidential

company’s

information from any unrelated parties.

•

Availability of information systems:

Availability relates to information and systems are being ready to use when it is

require by the management.

2.5.3 Internal

Controls in Information

Technology environment

(Green et al,

2006):

1. Development and implementation of information architecture in the

organization:

According to Cummings, information architecture refers to a “ rules and methods

that aim to identify and organize information in a purposeful and service-oriented

way” (Cummings, 2009). Maintenance and development of information overtime

is improved by having the implementation of information architecture.

|

|

35

2. Identification of potential and impact of business risk:

Management has to identify possibilities of potential risks result from

implementation of information systems that may happen in the, and also identify

the impacts that may affect the organization. In this way, the management will be

able to minimize loss related to the organization.

3. Existence of policies and standards regarding information system:

Policies and security standards have to be made in order to meet the objectives

and ensuring that workflow in the organization are according to the standards. By

implementing these policies will increase control in the business environment.

4. Existence of Procedures that regulate users:

Users of information systems need to be regulated as to create high control in the

IT environment. Therefore, procedures are made in order to regulate users of

information. Procedures are use to determine several important tasks in the

organization such as access of new users, unauthorized personnel, and terminated

employees from using the access.

5. Development of security standards to support the objectives of security

policy:

The aim of development of security standards is to assess whether the security

standards

have

meet the objectives of the policy.

By having this development,

the

management will be able to decide what needs

to be done if the standards

|

|

36

have

not

meet

the

objectives,

this

will

improve

the controls

in

the

IT

environment.

6. Implementation of Appropriate controls and vulnerability assessments:

The management has to ensure that implementations of controls are in an

appropriate way, and also independent assessment controls have been conducted

within a year

7. Limitation of access to confidential facilities:

Access to sensitive area or confidential facilities have to be restricted and it is

recommended to

have special security such as card or key reader,

finger that

is

useful to authenticate the users. Management also need to review user access

appropriateness based on their responsibilities.

2.6 Fraud

2.6.1 Definition of fraud

According to SAS 82, fraud is defined

as fraudulent actions that cause material

misstatement to the financial statement. “ Fraud is a serious threat to organization, it

can

take in

various action but

the

impact are all the same which

result

in

loss

of

value to the stakeholders” (Avellanet, 2010)

|

|

37

2.6.2 Actions of fraud:

Refer to Reinstein and Bayou, Actions of fraud differ from objects of fraud. Action

is an activity carried out by the individual such as stealing and misusing, while the

object is the target of the activity such as asset, inventory (Reinstein, Bayou, 1999).

However, Objects can be

in form of both tangible and intangible. Fraud action

is

classified into two, which are:

1.

Fraudulent financial reporting

Fraudulent

financial

reporting

is

an

intentional

financial

misstatement or

omission of amounts or disclosures with an intention to deceive users (Reinstein ,

Bayou, 1999). Actions of fraudulent financial reporting include:

(a) Manipulation and falsifying of data, transaction and record of activities

(b) Misrepresentation

or omitting

of events,

transactions and

other relevant

information

(c) Misapplication of accounting principles during recording activities

2. Misappropriation of assets

Misappropriation of assets is a fraud action, which involves theft or misuse of

company assets. The loss of company asset is an important management concern,

as this loss will bring unprofitable behavior for the company.

|

|

38

2.6.3 Motives of fraud

There are

various factor

that drives individual for committing

fraud. According

to SAS 82 (par 6),

motives of

fraud are classified

into two

factor, these

factors

are:

Motivation: Motivation is a form of pressures or initiative to commit fraud.

Refer to Reinstein and Bayou, SAS 82 has divided motivating factors into

two, which are:

1. Motivating factors to misstate financial statements:

The factors that drive individual to misstate financial statement include:

a.

Managerial

factors

pertaining

to

management's

abilities,

pressures,

style and attitude regarding internal controls and financial reporting

process.

b.

Industrial factors including economic and regulatory conditions

c.

Operating and financial factors from the nature of the company such

as, financial and profitability conditions.

2. Perceived opportunities

According to Robertson and Louwers (1999), “ an opportunity is an open

door for solving the problem in secret by violating a trust”.

Perceived opportunities are important factor that drives individual to

commit fraud.

|

|

39

|