24

APB 19 "Statement if Changes in Financial

Position"

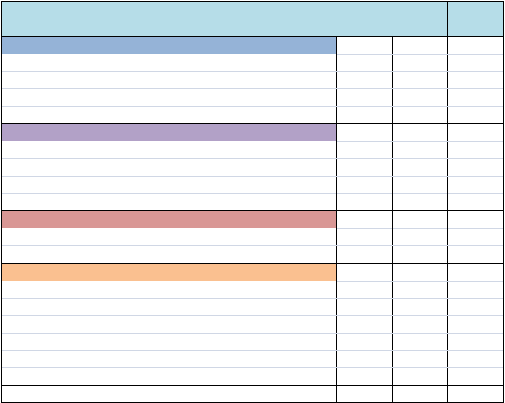

(CASH BASIS)

Funds From Operation

Profit

4

Depreciation

3

Total

7

Funds from Other Sources

New issue sources

5

New debt

2

Total

7

Application

Net Fixed Assets

7

Increase in Working Capital

Stock

4

Debtors

4

Creditors

-1

Dividend Paid

0.5

Tax paid

0.5

8

Total Applications

Increase

15

Total Applications Increase (decrease) in cash and near cash

-1

Table 2.5. “Statement of Changes in Financial Position”- Cash Basis

From: The Funds Statement: An Inquest, 1992

According to Donleavy (1992, p.28), due to the ambiguity and unclear

objective, FASB

decided

to

issued SFAS

95

“Statement

of

Cash

Flow”

in

November 1987. Statement of changes in financial position presented the

change

in

working

capital

rather

than cash

flows.

SFAS

95

clarify

the

main

purpose of statement of cash flow that is to report the cash flow which includes

the cash

inflows and outflow of an entity during a certain specified

which then

classified into three parts: cash flow from operating, investing and financing

over a reporting period. On

the other

hand,

the

term “fund”

was changed

into

“cash and cash equivalent” in accordance with the issuance of SFAS 95. When