29

2.3.2 Cash Flow from Investing Activities

When referring to IAS 7 paragraph 6 (International Reporting Standard 2005),

cash flow from investing activities is defines as “the acquisition and disposal of

long-

term assets

and

other

investments

not

included

in

cash

equivalents”.

Additionally,

investing activities are the second most

important activities

after

operating

activities.

The

investing

activities

associated with

acquiring

of

investments,

PPE

(property,

plant,

equipment)

and

lending

money

and

collecting the

loans (Weygandt

et all, 2005 p. 712). Generally, the

items

from

the investing activities resulted from the

changes

in

investment,

non-current

liability as well as shareholder’s equity items.

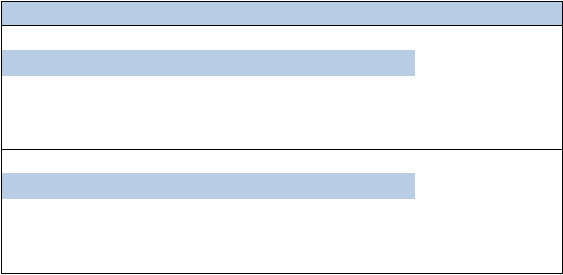

Investing Activities- Changes in Investments and Long Term Assets

Cash Inflow:

From sale of property, plant and equipment

From sale if debt or equity secutirites of other entities

From collection of principle on loans to other entities

Cash outflow:

To purchase property, plant and equipment

To purchase debt or equity securitites or other entities

To make loansto other entities

Table 2.7. Cash Flow from Investing activities

From: Accounting Principles, 2005