8

CHAPTER

II

BUSINESS

ANALYSIS

2.1

Industry Analysis

Poultry industry in Indonesia is the most advanced in the livestock sector. It

has

one

of

the

brightest

growth

prospects in

Indonesia.

60%

of

production is

concentrated in Java, with the balance distributed as follows: 30% in Sumatra, 6% in

Kalimantan

and 4% in Sulawesi. Its rapid growth is fuelled by a huge

market

potential and

the

relatively

low

consumption

on chicken

in

Indonesia compared

its

South East Asia neighbors as can be seen in the table below:

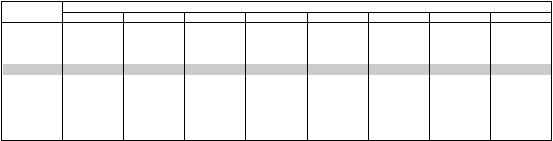

Table 2.1 : Chicken Consumption Per Capita in ASEAN Countries

Country

Year

1995

1996

1997

1998

1999

2000

2003

2004

Laos

Kamboja

Vietnam

Myanmar

1.9

1.5

1.7

2.3

1.9

1.7

1.9

2.6

1.9

1.7

2

2.8

1.9

1.7

2.1

3

1.92

1.65

2.22

3.42

1.93

1.68

2.3

3.48

1.95

1.81

2.62

3.64

1.97

1.87

2.74

3.82

Indonesia

4.4

4.6

4.4

2.9

3.27

3.45

3.92

4.22

Phillipines

Thailand

Singapore

Malaysia

Brunai

5.8

10.3

24.9

26

39.8

6.5

11.2

24.9

26.5

42.6

7

11.8

24.5

27

46

6.8

10.8

25

26

45

7.61

11.5

27.2

34.1

45.63

7.59

12.2

26.8

29.63

47.12

7.99

14.9

27.8

36.24

46.2

8.02

15.28

28

36.74

46.36

Source : FAO

In

Indonesia, poultry

industry

also

has

relatively

low

competitiveness and

profitability compared to poultry producers in other countries, notably USA, Thailand

|

9

and Brazil. The industry relies for almost 70% of its production inputs on imported

feedstuff and animal health care products like vaccines and others.

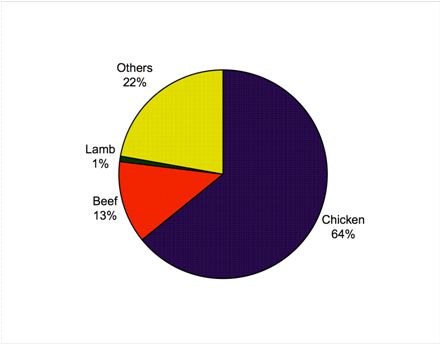

Based on the national meat consumption data for year 2003, chicken was at the

top

position,

which

is

64% of

total meat consumption,

far

higher than

other

meat

products,

such

as

beef

13%

and

lamb

1%

(chicken was

still

favorite

meat

for

Indonesians,

being

the

cheapest

source

of

animal protein and

for

a

predominantly

Moslem population, chicken is a key element of the meat diet).

Figure 2.1 : Indonesia’s Meat Consumption per Capita 2003

Source: FAO and Ditjen Peternakan

In year 2002 to 2004, the combined installed production capacity of feedmills

in Indonesia increases by an average of 3.6% p.a, from 5.5 million MT in 2002 to 5.7

|

10

million MT in 2003, and 5.3% p.a from 5.7 million MT in 2003 to 6.0 million MT in

2004. This is in line with the growth of chicken meat production.

Table 2.2

:

National Feedmill and Chicken Meat Production

2002

2003

2004

Feedmill Production

5.5

5.7

6.0

Chicken Meat Production

1.1

1.1

1.2

Source : FAO and Ditjen Peternakan

For a company to succeed in the poultry business, it needs to fully integrate its

upstream

and

downstream

operations.

This

comprises several

major

production

activities: feed production, DOC (Day Old Chick) breeding, chicken farming, chicken

dressing and processing, and distribution. In Indonesia, although there are more than

15 poultry operators, only 3 are fully

integrated. These are PT Charoen Pokphand

Indonesia Tbk, PT Japfa Comfeed Indonesia Tbk and PT Sierad Produce Tbk.

2.1.1

Competitor Analysis

2.1.1.1

PT

Charoen Pokphand Indonesia Tbk (Charoen

Pokphand)

Charoen

Pokphand

began

commercial operations

in

1972

with

feeds

production capacity of 20,000 tons a year in 2.4 hectares of land area in Jakarta. The

|

|

11

products consisted of, among others, cattle feeds (cow, pig) and poultry feeds (layers,

broiler and duck). In 1976 and 1979, the company expanded its operation to Surabaya

and Medan by setting

up factories with capacities of 24,000 tons and 80,000

tons a

year, respectively.

After

undertaking

several production

improvements, presently,

Charoen

Pokphand

has

annual continued

total

production

capacity of

650,000

tons

in

its

factories in Jakarta, Surabaya and Medan.. The factory in Jakarta has a land area of

27,284 square meters (with production capacity of 200.000 tons a year), Surabaya has

a land area of 42,565 square meters (with production capacity of 250,000 tons a year),

and

Medan

has

a

land

area of 17,595

square

meters (with production capacity

of

200,000 tons a year).

Witnessing the increase in the market demand for shrimp feeds, in 1988,

Charoen

Pokphand

expanded its

business

to

the

production

of

shrimp feeds

by

establishing a

factory

with a capacity of 40,000 tons a year

in Medan. To

further

strengthen

its

market position

in poultry

feeds, on April 24, 1990, the shareholders

approved

to

take over

80%

of

the shares of

P.T

Charoen Pokpand

Jaya

Farm, a

company domiciled in Jakarta and engaged in poultry and other animal husbandry.

Charoen Pokphand became a public (listed) company on 18 March 1991. In

2003,

despite sales

growth

of

9.93%

in

2003

and

11.31%

in

2002,

the

company

suffered a net loss of Rp 21.8 billion in 2003, and a profit of Rp 131 billion in 2002.

Appendix 4 shows the financial information in more details.

|

|

12

2.1.1.2

PT Japfa Comfeed Indonesia Tbk (Japfa)

Established on 18 January 1971,

Japfa became a public (listed) company on

23 October 1989. With total production capacity of 1.6 million tons per annum, Japfa

is one of the leading feed manufacturers in the country. Of the total feed produced by

Japfa

today, 10%

is used

for

internal

breeding operations

while

the

rest

is sold

to

local farmers and independent distributors.

Japfa

attributes

its

success

in

feed

production to

five

critical

factors:

a

sophisticated feed technology system, an excellent feed formulation strategy, a strong

raw materials procurement capability, a high capacity utilization rate, and

unrivalled

distribution network.

Japfa places equal emphasis on producing high quality feeds and maintaining

quality

consistency

of

its

feed.

It

boasts

of

an

advanced

feed

technology

system

which

enables

it

to

implement a

stringent

quality

assurance

program.

In

feed

formulation, it has a team of qualified nutritionists who are capable of tailoring to a

particular set of feed specifications. This capability is a major benefit to customers as

a precisely formulated feed produces the best results and is also cost efficient.

In

farming, Japfa enjoys

a

high

level of

integration with

its subsidiary, PT

Multibreeder Adirama Indonesia Tbk. Established in 1985 and publicly listed on the

Jakarta and

Surabaya

Stock

Exchanges

in

1994,

Multibreeder

currently

operates a

number

of

poultry

breeding

farms

to

produce

DOCs

located

throughout Indonesia.

Most of Multibreeder’s DOCs are sold to local commercial farmers.

|

|

13

In 2003, JPFA sales growth was 10.02% and 3.14% in 2002, and resulting a

profit of Rp 151.9 billion in 2003, and Rp 1,088 billion in 2002. Appendix 5 shows

the financial information in more details.

2.1.2

Bird Flu Outbreak

Bird

Flu outbreak,

which

posed

a

serious

threat

to

the

poultry

industry

in

Indonesia, in fact did not influence the national chicken production level in 2003 and

2004. Table

2.2 shows

that the

national

chicken production

has

an

increase

of

9%

YoY, from

1.1 MT

in

2003 to

1.2 MT

in 2004.

The consumer

demand decreased

slightly

when

the bird

flu outbreak was first announced.

Some

articles support this

information as shown in Appendix 7 to 9.

2.1.2

Commodity Price

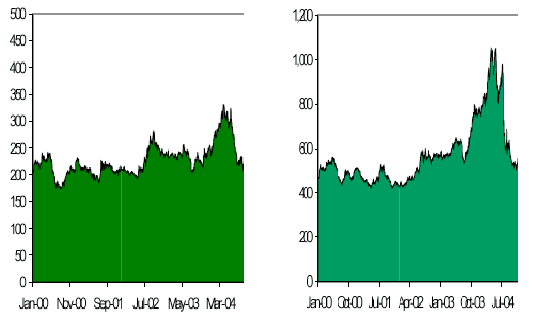

In poultry businesses, production cost is highly

influenced by the

fluctuation

in

raw material price, especially for two major commodities, corn and soybean meal

(SBM) as shown in Figure 2.2 below, which together account for about 70% of total

production

cost.

Most of

these are

imported,

and

therefore, are closely

related

to

exchange

rate

risk. The ability

to

take good

inventory position

and

forecasting,

and

the ability to transfer the increase of production cost to selling price are the major key

factors to success in this industry.

|

14

CORN

SBM

Figure 2.2 : Corn and SBM Price (in USD/bushel)

Source : Company Data

2.2

Company Analysis

PT Sierad Produce Tbk is an entity resulting from the merger in 2001 of four

companies conducting

the core

business

of

Sierad

Group.

These

were

PT

Anwar

Sierad

Tbk, PT Sierad Produce

Tbk, PT Sierad Feedmill

and PT Sierad Grains. Its

core

businesses

include the

production

of

primary

processed

and

poultry

feed,

breeding

and hatchery,

growing

farm,

slaughtering and production of

further

processed and value added chicken products, poultry equipment, fishmeal production,

|

|

15

fast

food and animal

health and pharmaceutical.

8

The company,

formerly PT

Betara

Darma Ekspor Impor, was incorporated on 6 September 1985. Its current

name was

adopted on 27 December 1996 in preparation

for its successful public listing on the

Jakarta Stock Exchange.

“Being

focused,

we

at

Sierad Produce would

like

to

be concentrated in

the

food related industry.

Our ultimate goal is for every Indonesian citizen to have the

opportunity and affordability to buy our products at very affordable prices, which is

actually to fulfill the dream of the Company to be one of the leading food companies

in Indonesia”, said Mr. Budiardjo Tek explaining the vision of the Company.

9

2.2.1

Business Description

2.2.1.1

Feedmill

Sierad Produce is recognized as one of the largest feeds producers in

Southeast

Asia,

with

state-of-the-art

facilities and

production

capacity

of

800.000

metric

tons per annum.1

0

Sierad Produce’s

feedmills,

located

in different

parts of

Indonesia,

are

computer-automated to

ensure

consistent

product

quality

and

operational efficiency at all stages of production.

Sierad

Produce’s

unique

competitive advantage,

stemming

from

its

use

of

expanders in

its production process,

ensures the

production of

hygienic, nutritious

8

The last two were divested in 2006

9

Quoted based on direct interview

10

PT Sierad Produce Tbk - Company Profile

|

|

16

and highly digestible feeds. It is not surprising then that Sierad feeds are the “feeds

of choice” for many chicken growers in Indonesia.

2.2.1.2

Breeding

Sierad

Produce

breeds

parent stocks

of

different strains,

which are

sourced

from foreign and local grandparent stockbreeders.

The parent stocks in turn produce

eggs that are then hatched to become the final stock of day-old-chicks (DOCs)

Sierad

Produce ensures the

production

of

high quality

DOCs

by

operating

modern closed-house breeding

farms,

fitted

with

tunnel ventilation, cooling

pads,

foggers and automated feeding and drinking systems.

Sierad Produce implements strict bio-security and vaccination programs in

its

breeder farms to ensure that the flocks are consistently disease-free.

Sierad Produce’s

breeding facilities produce up to 105 million DOCs every year.

2.2.1.3

Hatchery

For Sierad Produce,

“the art of hatching eggs

into healthy

DOCs”

is a noble

mission and a year-round pursuit. Sierad Produce’s hatchery operations adhere to the

highest standards and employ the latest technology and “best practices.”

|

|

17

Sierad Produce’s hatcheries use modern machines and equipment supplied by

well-known

international suppliers of setters and hatchers. Its

hatchery facilities are

capable of hatching up to 120 million eggs per annum.

2.2.1.4

Growing Farm

Sierad Produce raises the DOCs to become broiler chicken, either in the more

modern company-owned closed house farms or through contract growers who largely

use the more traditional open-houses.

As in its breeding farms, Sierad Produce also

employs strict bio-security and vaccination programs in

its

final stock broiler farms.

Sierad Produce constantly motivates and assists its contract growers to increase their

net income by educating them and assisting them to exceed company-set productivity

standards such as feed conversion ratio, mortality, body weight and growing days.

Sierad Produce’s partnership with its contract growers plays a vital role in the

nation’s

socio-economic development,

most

especially

in

the

countryside.

Sierad

Produce

provides

its

contract

growers

with

the

full

package

of

production

inputs,

such

as,

day-old-chicks,

feeds,

poultry

health

care

products,

technical

assistance

as

well as education in the

latest

farm management techniques. Sierad Produce finally

provides the

logistical

support

to

ensure

the

efficient

distribution

of

full-grown

chicken when they are ready for harvest.

Sierad Produce helps elevate the income and the quality of life of

its contract

growers,

their

families

and

other

dependents

by providing them

those production

|

|

18

inputs and

capital

goods,

which

would have otherwise been

unaffordable or

inaccessible for many of them.

2.2.1.5

Slaughterhouse & Poultry Food Processing

Sierad

Produce’s

slaughtering

facilities are

among

the

most

modern

and

hygienic in the

country.

The

facilities and processes are

HACCP-certified. Sierad

Produce has slaughtering capacity of 8,000 chickens per

hour. The complex process

involves scalding,

plucking

and

eviscerating,

cutting,

deboning

and

chilling

or

freezing. Sierad Produce strives to optimize its profits by continuously creating added

value thru the entire value chain of primary and further processing. Sierad Produce

ensures that all of its processes and procedures conform to the “halal” requirements.

Sierad Produce

takes

pride

in the

quality of

its dressed chicken

and

further

processed

products,

and

for

which

it

has

become the

“supplier

of

choice” for

the

overwhelming

majority

of

international franchised

fast

food

chains

operating

in

Indonesia.

2.2.1.6

Fast Food

Sierad

Produce

has

a

two-faceted

involvement in

the

retail

food

industry,

firstly

through its exclusive franchise for Wendy’s Indonesia, and secondly through

|

|

19

its

exclusive

license

for American-based

Hartz “all

you can

eat”

chicken

buffet

restaurants for Indonesia and selected countries in Asia.

2.2.1.7

Supporting Operations

Sierad

Produce

operates

sophisticated laboratories

in

various

parts

of

the

region

to

help ensure

that

only

high

quality

products are

produced

at

each

of

its

facilities: feedmills, breeding farms, hatcheries, broiler farms, slaughtering and

further

processing.

Sierad

Produce

also

produces

plastic

poultry

equipment using

injection and

blow

techniques for

automatic

drinkers,

feed

pans and

other

similar

poultry equipment, and animal health care and pharmaceutical product, to supply the

internal

requirements of

its

breeding

and

contract

farms

as

well

as

those

of

independent farmers

2.2.2

SWOT Analysis

This

analysis

involves monitoring

the

external

and

internal

marketing

environment. Once the Company has performed a SWOT analysis, it can proceed to

develop specific goal for the planning period.

The analysis starts from the determination of key strengths of the Company:

1. Integrated Business Strategy

|

|

20

With

vertical

integrated

business,

the

company

will

be

more

competitive,

and

have better supply and distribution chain since all units can support the operation

of each other.

2. Available Capacity

The company still has enough capacity to increase their production volume in the

future. The feedmill’s capacity is one of the largest in South East Asia, while its

Slaughterhouse is

one

of

the

most

modern

and

largest

in

Indonesia,

with

slaughtering capacity of 8.000 birds per hour.

3. Bio Security System

The company has implemented

strict bio security system to ensure that the

product is hygiene, healthy and safe to be consumed.

4. Halal and HACCP Certification

Through

this

certificate,

the

product

could

be

consumed

by

every

people

and

could meet the international standard for fast food operators.

5. ERP System

The company had collaborated with Microsoft Indonesia to implement Microsoft

AXAPTA for better reporting, planning and controlling.

Instead, with the current situation, the Company faced some problems, which

put it in the weak position such as:

1. Slow Corporate Growth

One

of

the

reason why

corporate

grew slow

was

lack

of

working

capital.

The

Company ran the business only by internal financing. It could not get any external

|

|

21

source of financing, while

the obligations

to

the

Bondholders and Lessors

were

still outstanding.

2. High Financing Cost

Since the Company has a good relationship with some suppliers, the company is

allowed

to

get

financing

from

suppliers.

However,

the

cost

become higher

compared to the Bank loan, since the suppliers take a higher margin.

However, this weak position has challenged the Company to find the ways for

improvement and to grab the following opportunities in order to increase its sales in

the future, considering that it still has some key strength to be further developed:

1. Increasing Demand for Modern Slaughterhouse

As

result

from

Bird

Flu

disease, some people are

more

concern about healthy

chicken, and therefore, it is possible to increase the production level in the future

due to the increase of demand, where the product has met the required standard.

2. Limited local brand for dressed chicken

The

brand

of

Sierad’s

dressed

chicken is

“Delfarm”.

Since

there

are

seldom

branded chicken in the market, it is an opportunity for the Company to built brand

awareness and treat the product in an exclusive one that offer

value added to the

consumers, compared to the

other

similar

product.

(Considering

that chicken

is

commodity product)

3. Low poultry consumption Level

As

mentioned earlier,

the chicken

consumption

level

per capita

in

Indonesia

is

low compared to other countries

in South

East Asia.

Since

the

level of

|

|

22

consumption

is closely related with

the

GDP rate,

it

means that if

the

income

(GDP) level in Indonesia is increase, so the demand of chicken will increase too.

Besides strength,

weaknesses,

and

opportunities,

the

Company

was

also

threatened by some factors as follows:

1. Increasing Raw Material and Energy cost

Fluctuation in raw material price, especially for imported ones, and an increase of

energy

cost

are

two

major

threats

for

the

company to

become

competitive

compared to the others.

2. New Entrance

New

entrance that

comes with

sufficient

working

capital,

facilities,

knowledge

and skill can threaten the company to maintain its current position.

2.2.3

4

P

Analysis

The 4 P analysis

is

important to determine the

marketing objectives of the

Company and strategies to be taken

in order to increase the sales (Kotler, 2006, p.

245). The components are product, price, place and promotions.

For product, although the Company produces commodity type product, it has

own brand, to differentiate the products to other competitors’ and to give value added

to the customers.

The Company’s strategies to develop its products are as follows:

1. To increase brand awareness, through advertising, campaign, etc.

|

|

23

2. Product Differentiation and Segmentation based on income level and customer’s

target. For example, the

low-end

customer

in

selected area

will

prefer

to

buy

cheaper product rather than product with premium price.

3. Customer satisfaction monitoring

Regular monitoring is very important in order to know whether the products are

acceptable, and the existing customers are willing to repeat the order.

4. Research and Development to create innovative product.

For pricing, the Company uses the 2 strategies as follows:

1.

To implement premium pricing

for superior product and

at par

pricing for

the

standard one.

It means that the pricing strategy is closely related to the quality of product.

2. To monitor profit margin per product, per customer, and per distribution channel.

The company also has distribution (place) strategies as follows:

1. To open new branch which have closer access to the market in order to reduce the

distributor’s role.

2. To expand the distribution channel in both modern and traditional market.

Promotion strategy

also

takes an

important

role,

since

even

though

the

Company can produce qualified product, competitive pricing and distribution place,

without

good promotion

strategy,

it can

not

successfully

obtain

its

goal. Therefore,

the Company has taken promotion strategies as follows:

|

24

1. Customer acquisition by increasing brand awareness and product differentiation,

and also customer retention by maintaining the best quality and creating incentive

program.

2. To

implement Key

Account

Management

Concept

in

order

to

give

optimum

service to the customers.

2.2.4

Financial Performance

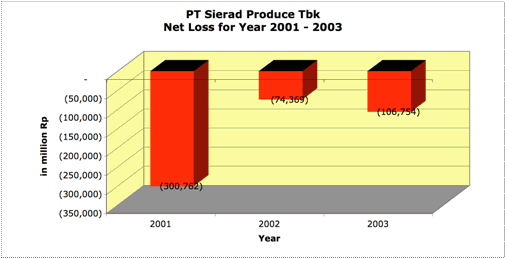

The company’s sales growth was -14.4%

in 2003 and 0.60%

in 2002 which

resulting a net loss in

the sum of Rp 106.8 million in 2003 and

Rp 74.3

million in

2002.

Figure 2.3 : Net Loss For Year 2001 - 2003

|

25

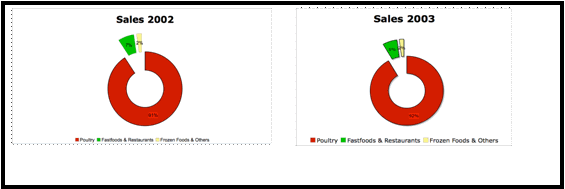

The proportion of sales in 2002 and 2003 are as follows:

Figure 2.4 : Proportion of Sales 2002 - 2003

Source : Company’s Annual Report 2002-2003

Earning

from

operations

before

interest,

taxes,

depreciations and

amortizations (EBITDA) fell from Rp 62.1 billion

in 2002 to just under Rp 1 billion

in 2003. Operating income also declined, from Rp 21.1 billion in 2002 to losses of Rp

41.8 billion in 2003.

For

financial

ratios,

current

ratio

was

remained

unchanged at

3.4:1.

Shareholder equity rose from Rp 74.78 billion to Rp 205.34 billion, due to fixed asset

revaluation

of

Rp

237 billion.

Solvency

improved

considerably:

the

debt

to

equity

ratio

improved

from 14.4:1

in 2002 to 5.2:1 in 2003, and debt to total

assets from

0.93:1 to 0.84:1.

Below

is financial ratio comparison between the

Company and its

competitors, PT Charoen Pokphand Indonesia Tbk and PT Japfa Comfeed Indonesia

Tbk:

|

26

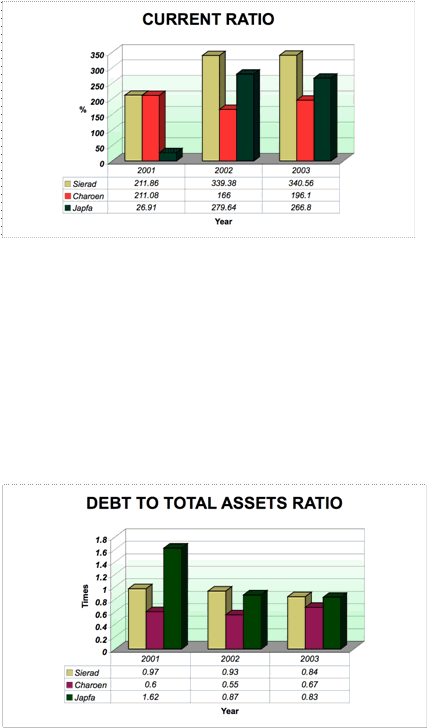

Figure 2.5 : Comparison – Current Ratio for Year 2001 – 2003

The

above

comparison

shows

that

the

current

ratio

of Sierad

was

higher

compared to Charoen and Japfa, which is 211.86 percent in 2001, 339.38 percent in

2002, and 340.56 percent in 2003. It means that in term of liquidity, Sierad was more

liquid compared to its competitors for year 2001 – 2003.

Figure 2.6 : Comparison – Debt to Total Assets Ratio for Year 2001 – 2003

|

27

It

shows

that for

Sierad,

the proportion of debt

to

total assets

was

0.97

in

2001, 0.93 in 2002, and 0.84 in 2003, which was

higher than

its competitors in the

same

period. It

means

that Sierad

used more debt

to

finance

its assets,

rather than

equity.

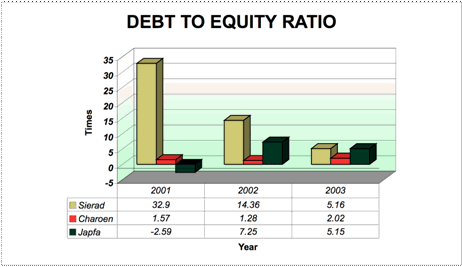

Figure 2.7 : Comparison – Debt to Equity Ratio for Year 2001 – 2003

It shows that for Sierad, the comparison of the amount of debt financing to the

amount of equity financing was higher than its competitors, which was 32.9 times in

2001, 14.36 times in 2002 and 5.16 times in 2003.

|

28

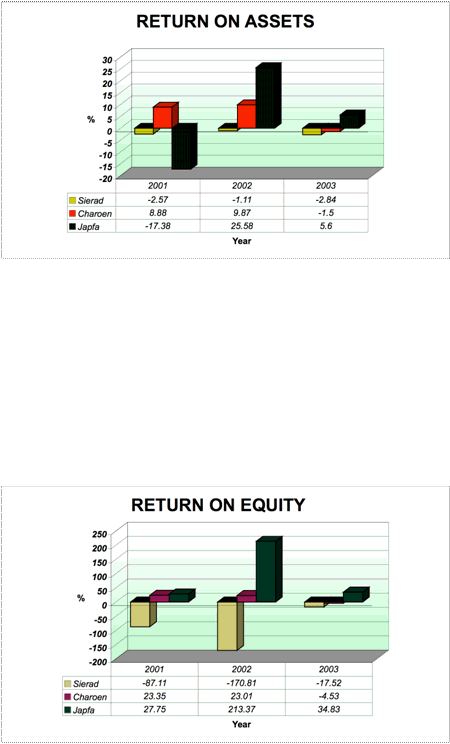

Figure 2.8 : Comparison – Return on Assets for Year 2001 – 2003

For Sierad,

the amount

of profit (net

income) produced

for a given

level

of

assets showed

negative amount, since the Company did

not book profit during

that

period. The percentage was lower than its competitors, except the one in 2001, where

Japfa was the highest, resulting from loss of Rp 494 billion in that period.

Figure 2.9 : Comparison – Return on Equity for Year 2001 – 2003

|

|

29

The purpose of this ratio is similar to that of the return on assets ratio, except

that it

focuses on the owner’s initial investment (represent by the equity) rather than

total assets.

Based on

the above

information, it shows

that the return

of

equity

of

Sierad was lower compared to its competitors.

The details of financial information are shown at Appendix 6.

|