14

increases

in equity,

other

than increases

relating

to

contribution

from equity

participants.”

Last, when

refer

to the

IASB Framework paragraph 70 (International Financial

Reporting Standard 2005), expenses are defined

as

“decreases

in

economic

benefits

during

the

accounting

period

in the

form

of

outflows

or

depletion

of

assets

or

incurrence

of

liabilities

that

results

in decreasing

equity,

other

than

those relating to distribution to equity

participants”.

Next,

based

on

IAS

paragraph 88 paragraph 1 (International Financial Reporting Standard, 2007) it

is

necessary for an entity

to present their analysis of expenses

in

the classified

form that is either by their nature (for example: employee benefits,

depreciation, transport costs, purchases of

material

and

advertising

cost)

or

based on

their

function

in

the entity such as cost of

sales, costs of distribution

and

administrative activities whoever provide more relevant and reliable

information.

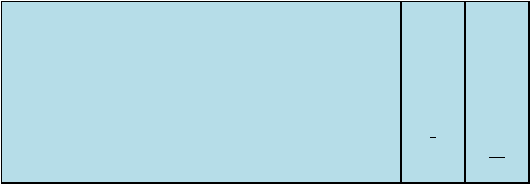

Revenue

x

Other Income

x

Changes in Inventories of finished goods and work in progress

x

Raw materials and consumables used

x

Employee benefit costs

Depreciation and amortisation expense

x

x

Other expenses

x

Total Expenses

(x)

Profit

x

Table 2.2: Example of classification of expenses by NATURE provided paragraph 91 of IAS 1

From: Applying International Accounting Standards (2005), page 567