15

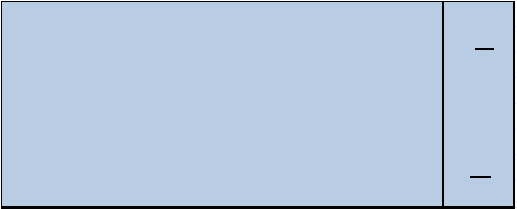

Revenue

x

Cost of Sales

(x)

Gross profit x

Other income

x

Distribution costs (x)

Administrative expenses (x)

Other expenses

(x)

Profit

X

Table 2.3: Example of classification of expenses by FUNCTION, based on expense method

provided in paragraph 92 of IAS 1.

From: Applying International Accounting Standards (2005), page 568

Conversely when referring to Alfredson

et

al

(2005,

p.68),

the

definition

of

expense

itself

include

both

losses

and

expenses

that

result

from an

ordinary

course of an entity. While

losses represent other

items that

meet the definition

of expenses and

may or

may

not occur

from in the

route of economic activities

of an entity.

2.1.3 Statement of Changes in Equity

Changes

in owner’s equity during the specified period of

time such as a

month

or a year are being summarized in the statement of changes of equity (Hongren

& Harrison, 2007 p.19). To what we can

summarize, there are several factors

affecting

the

decrement

or

increment in

owner’s

equity.

Factors

such

as

investments

made

by

owner

and

the

net

income

can

caused owner’s

equity

to

increase.

On

the

other

hand,

things

such

as

net

loss

and

owner

withdrawals

may lead to the decrement of owner’s equity. In addition, when refer to