84

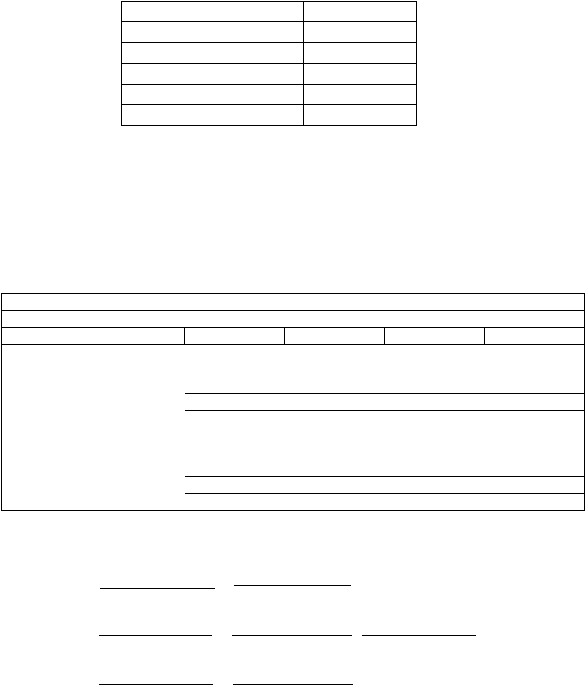

Tabel 4.33. Pertumbuhan

DEWA

2007 - 2010

Sales

0,60%

Operating income

1,69%

Capital Expenditure

14,38%

depreciation

32,03%

Working Capital

68,59%

Sumber: hitungan penulis

Untuk

mencari

nilai

interinsik

tahun

2009

dan

2010.

penulis

menggunakan

data

actual

dan forecast.

Nilai

interinsik

untuk

DEWA

tahun

2009.

2010.

dan 2011

dijabarkan sebagai berikut:

Tabel 4.34. Estimasi Arus Kas DEWA Tahun 2009

DEWA

Estimasion Of Free Cash flow

2009 (actual)

2010 (actual)

2011 (forecast)

2012 (forecast)

Sales

Operating income

Less: tax

Net operating profits after tax

Plus: depreciation expense

Less investments:

In net working capital

In new capital (CAPEX)

Total net investment for the period

Free cash flow

1.894.100.000.000

2.050.421.100.000

2.591.358.656.357

3.275.005.161.561

30.140.800.000

35.792.200.000

667.978.770.713

844.203.451.550

7.535.200.000

8.948.050.000

166.994.692.678

211.050.862.887

22.605.600.000

26.844.150.000

500.984.078.035

633.152.588.662

1.198.500.000.000

1.273.381.900.000

1.548.913.728.824

1.884.064.583.721

(107.160.000.000)

947.239.300.000

336.021.208.982

424.669.580.612

74.410.100.000

71.584.400.000

113.927.779.043

143.983.953.551

(32.749.900.000)

1.018.823.700.000

449.948.988.026

568.653.534.164

1.253.855.500.000

281.402.350.000

1.599.948.818.834

1.948.563.638.219

Sumber: hitungan penulis

WACC=

8,94%

terminal value =

free cash flow

2012

=

1.948.563.638.219

= 21.788.914.718.820

k

wacc

8,94%

firm value =

1.253.855.500.000

+

281.402.350.000

+

1.599.948.818.833

+

(1+8,94%)1

(1+8,94%)2

(1+8,94%)3

1.948.563.638.219

+

21.788.914.718.820

(1+8,94%)

4

(1+8,94%)

4

=

1.253.855.500.000

+

281.402.350.000

+

1.599.948.818.833

+

1.948.563.638.219

+

21.788.914.718.820

firm value =

19.476.928.530.881

Setelah firm value diketahui. maka proses selanjutnya mencari share value.