95

(1+16,21%)

4

(1+16,21%)

4

=

(1.122.666.150)

+

2.877.327.950

+

1.617.237.699

+

1.971.618.542

+

12.162.934.988

firm value =

5.683.920.237

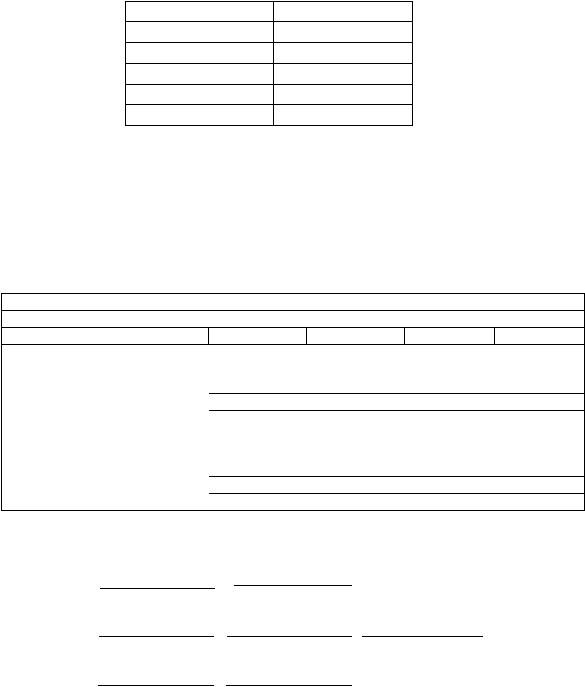

Tabel 4.52. Pertumbuhan

INDY

2007 - 2010

Sales

19,30%

Operating income

15,21%

Capital Expenditure

28,28%

depreciation

45,87%

Working Capital

59,11%

Sumber: hitungan penulis

Setelah asumsi untuk tahun 2009. 2010. dan 2011 diketahui. maka selanjutnya akan

dicari nilai interinsiknya.

Nilai interinsik untuk INDY tahun 2009. 2010. dan 2011

dijabarkan sebagai berikut:

Tabel 4.53. Estimasi Arus Kas INDY Untuk Tahun 2009

INDY

Estimasion Of Free Cash flow

2009 (actual)

2010 (actual)

2011 (forecast)

2012 (forecast)

Sales

Operating income

Less: tax

Net operating profits after tax

Plus: depreciation expense

Less investments:

In net working capital

In new capital (CAPEX)

Total net investment for the period

Free cash flow

2.486.579.600

3.765.467.000

4.758.864.170

6.014.337.182

612.383.000

619.653.000

1.226.700.222

1.550.325.559

153.095.750

154.913.250

306.675.055

387.581.390

459.287.250

464.739.750

920.025.166

1.162.744.169

1.009.754.700

1.252.501.300

1.523.515.026

1.853.170.161

2.486.579.600

3.606.366.300

617.081.425

779.878.480

105.128.500

988.202.700

209.221.068

264.417.307

2.591.708.100

4.594.569.000

826.302.493

1.044.295.787

(1.122.666.150)

(2.877.327.950)

1.617.237.700

1.971.618.543

Sumber: hitungan penulis

WACC=

16,21%

terminal value =

free cash flow

2012

=

1.971.618.542

=

k

wacc

16,21%

12.162.934.988

firm value =

(1.122.666.150)

+

2.877.327.950

+

1.617.237.699

+

(1+16,21%)1

(1+16,21%)2

(1+16,21%)3

1.971.618.542

+

12.162.934.988

Setelah firm value diketahui. maka proses selanjutnya mencari share value.